GST 2.0 Reforms: Simplifying India's Indirect Tax Landscape

GST 2.0 marks the second phase of India's indirect tax evolution, aimed at simplifying rates, improving compliance, strengthening fiscal federalism, and driving domestic demand through a rational, technology-enabled tax structure.

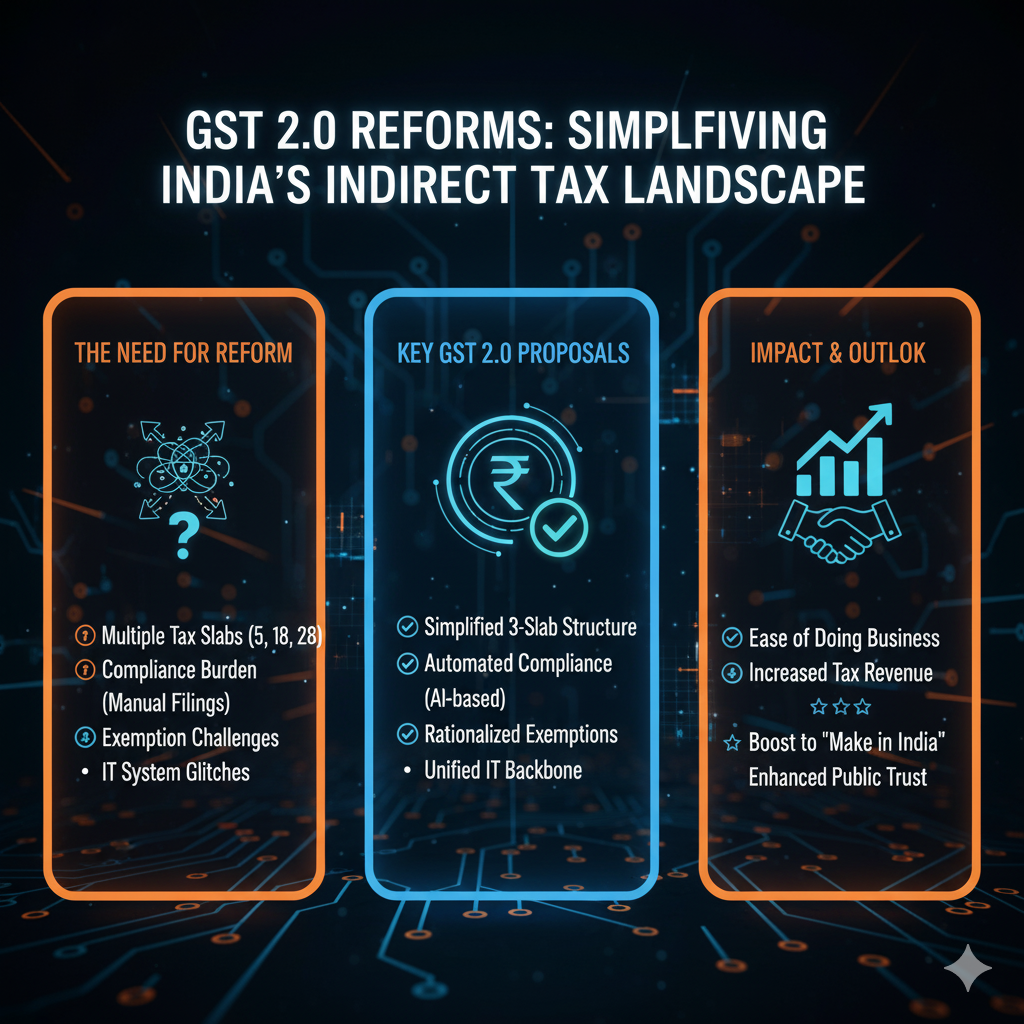

Introduction

GST 2.0 represents India's attempt to refine its path-breaking indirect tax reform introduced in 2017. Positioned as the ‘next-generation GST’, it addresses structural frictions, slab complexity, inverted duty issues, and fiscal federalism concerns, while leveraging digital architecture for trust-based, seamless tax administration.

Context & Background

India's GST was built on the vision of “One Nation, One Tax, One Market”. After 8 years of implementation, improved tax buoyancy and compliance maturity provide fiscal space for structural rationalisation. With compensation cess expiring in 2025 and global trade headwinds rising, GST 2.0 aims to boost domestic consumption, enhance investor confidence and strengthen cooperative fiscal governance.

Key Points

- •Simplified Three-Tier Rate Structure: Transition from 5 slabs to 3 (5%, 18%, 40%), reducing ambiguity, classification disputes and litigation burden — a step closer to global VAT trends.

- •Fiscal Federalism Balancing Mechanism: With compensation cess ending, GST 2.0 explores formula-based revenue support frameworks, stabilisation funds and periodic review mechanisms for states with weaker fiscal capacity.

- •Correction of Inverted Duty Structures: Focus on textiles, footwear, EV components and agro-machinery sectors to ensure value-added production competitiveness and reduce working capital lock-ins.

- •Targeted Relief for Priority Sectors:

- Health & insurance — reduced cost burden, enhancing affordability

- Renewable energy — tax cut aligns with India's net-zero agenda

- Real estate — reducing input cost improves housing affordability

- •Strengthening Digital Governance: AI-based audit flags, automated ITC reconciliation, e-invoicing deepening to MSMEs, expanding Aadhaar-PAN–GSTN triangulation for fraud control.

- •Boosting Domestic Consumption: Lower GST on consumer goods, building materials and insurance increases household disposable income — key during global trade contraction & tariff pressures.

- •Formalisation Push: Simpler rules & automation ease compliance for MSMEs, improving invoice-based credit trail and tax base expansion.

- •Green Transition Incentives: Lower duty on renewables & EV ecosystem supports India's climate financing commitments and energy diversification strategy.

- •Ease of Doing Business & Investor Confidence: Predictable rate regime, clarity in classification & reduced inspector-raj tendencies builds tax certainty — critical to attract global manufacturing.

- •Judicial & Institutional Reforms: Strengthened appellate mechanism, faster refund settlement architecture, tech-enabled taxpayer services to reduce disputes and improve trust.

- •Complementing External Sector Stress: GST relief acts as domestic stimulus to counter external tariff shocks (e.g., US tariff hikes), ensuring macroeconomic resilience.

Related Entities

Impact & Significance

- •Demand-Led Growth: Lower consumer taxes → higher spending → manufacturing uptick → employment generation.

- •Improved Fiscal Efficiency: Enhanced compliance and stable rate design improve tax buoyancy and certainty.

- •Boost to Infrastructure & Housing: Lower GST on cement and input materials reduces project costs, stimulating capex cycle.

- •Strengthening Cooperative Federalism: New compensation design & council-driven consensus reinforce trust in fiscal institutions.

Challenges & Criticism

- •Partial Rate Simplification: Three-tier structure still diverges from global single-rate VAT best practice.

- •Petroleum Exclusion: Keeping fuel outside GST creates inflation spillovers and tax cascading.

- •MSME Concerns: Higher GST on labour contracts risks margin stress in labour-intensive sectors.

- •State Revenue Anxiety: Compensation expiry risks fiscal friction without robust transition formula.

Future Outlook

- •Move toward 1-2 GST slab regime in long-term.

- •AI-driven audit & risk-based compliance replacing manual scrutiny.

- •Consider phased integration of petroleum, electricity & real estate.

- •Institutional strengthening of GST Council for dispute resolution.

UPSC Relevance

- • GS-3: Government budgeting, taxation reforms, formalisation, cooperative federalism

- • GS-2: Centre-State fiscal relations, institutional mechanisms (GST Council)

- • Essay: Fiscal prudence vs welfare, tax reforms & trust-based governance

Sample Questions

Prelims

With reference to GST 2.0 reforms in India, consider the following statements: 1) GST 2.0 introduces a three-slab structure. 2) Petroleum products are now under GST. 3) GST Council continues as the decision-making body for rates.

A. 1 and 2 only

B. 1 and 3 only

C. 2 and 3 only

D. 1, 2 and 3

Answer: Option B

Explanation: Petroleum remains outside GST; Council retains authority.

Mains

Discuss how GST 2.0 reforms seek to deepen tax rationalisation, enhance cooperative federalism, and strengthen India’s domestic demand-led growth strategy.

Introduction:

GST 2.0 reflects India’s shift from rollout-stabilisation to structural optimisation, driven by rate simplification, digital enforcement and fiscal equity between Union and states.

Body:

• Tax Rationalisation: Simplified slabs, correction of inverted duty structures, sectoral reliefs, automated credit chain → efficiency & lower compliance cost.

• Strengthening Cooperative Federalism: Compensation cess transition frameworks, empowered GST Council, transparent settlement cycles → reinforce fiscal trust.

• Boosting Domestic Demand: Lower GST on essentials, housing & renewables → stimulate middle-class spending, improve affordability & sustain growth amid global slowdown.

• Challenges: Petroleum exclusion, MSME tax pressures, state revenue uncertainty, need for single-rate alignment.

Conclusion:

GST 2.0 is a calibrated step toward a globally benchmarked VAT design. Its success hinges on balancing state autonomy with unified tax vision and leveraging technology for trust-based compliance.